How to Reconcile Multi-Payment Gateway Payouts for Shopify Sellers

Topic 1: The Diagnostic Hook & Net Deposit Error

Are you recording your Shopify net deposits as Revenue? If so, you are committing a GAAP violation that corrupts every margin calculation your business relies on. Here is why your books are lying to you and the exact architectural fix.

The distortion starts the moment a Shopify merchant adds a second payment gateway.

Topic 2: The Multi-Gateway Schedule Fragmentation

When a merchant adds Shopify Payments, PayPal, Stripe, and a Buy Now Pay Later platform like Klarna alongside each other, the cash coming into the business stops flowing in a single clean stream. Each processor runs on its own settlement schedule, each calculates and deducts fees before transferring anything to the bank, and each produces a deposit number that corresponds to no single day of sales.

A deposit landing in the bank on a Tuesday might represent a portion of Friday’s Shopify Payments sales, a swept PayPal balance, and a BNPL batch covering orders from the entire prior week, all compressed into one number sitting in the bank feed. Under accrual accounting, revenue must be recognized on the day a sale occurs, and that timing rule creates an immediate conflict with how gateways actually operate. Daily reconciliation at the transaction level breaks down in this environment, and that is precisely where the first distortions enter the financial statements.

Topic 3: The True Cost of Hidden Gateway Fees

The more immediate problem lives at the fee level. Every gateway deducts its processing fees at the source, before the wire ever leaves their system. When a customer checks out for one thousand dollars, the processor takes its cut, typically two point nine percent plus thirty cents, and nine hundred seventy dollars arrives at the bank. If the bookkeeper records that net deposit as revenue, the income statement simultaneously understates gross sales and understates operating expenses, violating GAAP and corrupting every downstream margin calculation the business depends on.

Shopify Payments charges processing fees ranging from one point five to two point nine percent plus a fixed transaction fee based on the merchant’s active plan. For third-party gateways like standard Stripe or PayPal, Shopify layers an additional platform transaction fee on top of the gateway’s own processing rate. And here is where the operational complexity compounds: that additional Shopify platform fee does not come out of the gateway payout. It bills separately on the merchant’s monthly Shopify subscription invoice. Three numbers now exist in parallel, the gateway settlement report, the Shopify dashboard, and the monthly invoice, and none of them naturally reconcile against each other without a deliberate accounting structure to bridge them.

Shopify also deducts monthly subscription charges and app fees directly from the first Shopify Payments payout of each calendar month. That specific deposit runs smaller than every other payout the business receives that month, and if the accounting system isn’t watching for it, that variance either gets flagged as an error or coded incorrectly into the wrong period.

Topic 4: Global Brands & Currency Exchange Leakage

Global brands selling across currencies absorb an additional source of ledger distortion at every international transaction. When a customer purchases in Euros and the merchant’s base currency is US dollars, Shopify records the transaction at the exchange rate active at the moment of checkout. The gateway then converts and settles the funds later, applying its own conversion rate plus a foreign exchange markup, as Shopify Payments charges one point five percent for US-based stores and approximately two percent on international sales for other regions.

The spread between the checkout rate and the payout rate produces a direct currency exchange gain or loss on every international order, and if those variances aren’t isolated in the books, the distortion absorbs silently into gross margins without anyone catching it. Merchants on Shopify Advanced or Shopify Plus can establish multi-currency payouts across up to eight distinct bank accounts, but that structure requires managing and reconciling separate foreign currency clearing ledgers for each account.

Topic 5: The Post-Fulfillment Financial Lifecycle

The financial lifecycle of an e-commerce transaction does not close at fulfillment. Refunds, partial refunds, and chargebacks continuously alter the net receivable balance across every active gateway. When a refund processes, the gateway reverses the original transaction but almost never returns the original processing fees. That fee loss deducts silently from the next payout rather than appearing as a visible line item in the current period. Partial refunds on multi-item orders require itemized adjustments to prevent the artificial inflation of net sales within a specific financial period.

Chargebacks strike faster: when a customer files a dispute, the gateway immediately debits the disputed amount from the next payout alongside a standard dispute fee of fifteen dollars, and the cash sits in a reserve status until the dispute resolves. A merchant win requires a complex reversal entry on the ledger; a merchant loss gets written off as a sales return or bad debt. Every one of those outcomes hits the clearing account differently, and none of them show up cleanly in the bank feed without structured accounting to catch them.

Topic 6: The Shop App Sales Tax Variance

One additional reconciliation variable catches merchants off guard consistently: the Shop App. Shopify now operates as an official marketplace facilitator for orders placed through the Shop App, meaning it calculates, collects, and remits sales tax directly to tax authorities on those specific transactions.

For orders placed through the standard online store, Shopify pays the sales tax out to the merchant, who stays responsible for filing. If the accounting integration fails to separate these two categories, the liability accounts overstate what the business actually owes, and tax filings end up inaccurate as a direct consequence.

Topic 7: The Ideal 3-Tier System Data Architecture

The solution to every problem described above runs through the same architectural decision: stop syncing individual transactions into the accounting general ledger and start syncing batched settlement summaries. This distinction matters enormously at scale. Direct order-level syncing, where the integration creates an individual invoice or sales receipt in QuickBooks Online or Xero for every Shopify order, is highly discouraged for any store processing more than one hundred orders per month. At that volume, the approach risks exceeding API transaction limits and corrupting database performance in the accounting software. The general ledger becomes clogged, reconciliation takes longer, and the system slows down as the transaction count compounds month over month.

The correct architecture removes individual transaction imports from the equation entirely. Shopify captures every checkout event and routes payment to the appropriate gateway, including Shopify Payments, PayPal, Klarna, and Stripe, each of which deposits net settlements into the corresponding bank account. An automated middleware connector sits between Shopify and the accounting software, pulling raw payout and order data from Shopify, translating it into clean, batched journal entries that separate gross sales, fees, taxes, and adjustments, and posting those structured summaries directly to QuickBooks Online or Xero. The accounting software receives organized, reconcilable data rather than raw transaction noise, and the general ledger stays clean regardless of order volume.

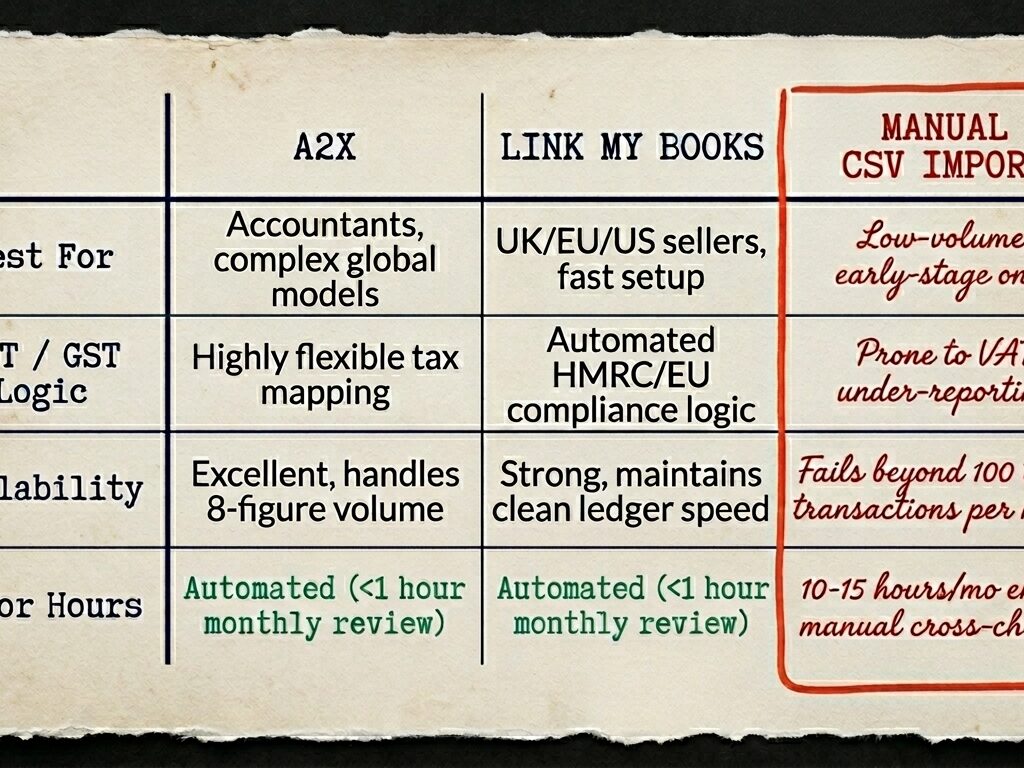

Topic 8: Middleware Comparison Matrix

Two platforms dominate this middleware category: A2X and Link My Books. A2X leans toward high customization and deep mapping control, making it the stronger fit for accountants managing complex global business models or merchants with non-standard revenue structures. Link My Books offers more standardized, out-of-the-box outputs with automated tax compliance logic built for HMRC and EU requirements first, which makes it the faster deployment for UK, EU, and US sellers who want clean summaries without heavy configuration.

Manual CSV imports, which represent the third option, fail practically beyond one hundred to one hundred fifty transactions per month, carry a high error rate, and become retroactively difficult to correct. Stores processing more than one hundred orders per month should not be running direct sync integrations, because that approach risks exceeding API transaction limits and corrupting database performance inside the accounting software.

Topic 9: The Balancing Clearing Account Pattern

The structural cornerstone of the entire system is the clearing account pattern. A clearing account sits on the balance sheet as a current asset, acting as a temporary holding space for funds in transit between the sale event and the bank deposit. When a sale occurs, the receivable enters the clearing account rather than flowing directly to a revenue account.

When the net payout arrives at the bank, the clearing account reduces by the corresponding gross transaction value, and the fee differential transfers to the profit and loss statement as an operating expense. Executed correctly, the clearing account balance drops to zero after every payout cycle. A non-zero balance at the end of a reconciliation period is a diagnostic signal pointing directly at an unrecorded adjustment, such as a missed refund, an open chargeback reserve, or a processor-held reserve that never got posted.

The gateway-specific clearing account structure should mirror the business’s gateway list exactly: a Shopify Payments clearing account, a PayPal clearing account, a Klarna clearing account, and a Stripe clearing account, each sitting on the balance sheet as a separate current asset. Funds flow through them independently, which makes it possible to isolate timing differences, fee discrepancies, and reserve balances at the gateway level without cross-contamination between processors.

Topic 10: Step-by-Step Blueprint (The Operational Journal Entries)

Let’s walk through a concrete example. A single day of sales totaling ten thousand dollars processes through Shopify Payments, carrying two hundred ninety dollars in processing fees, a one hundred fifty dollar chargeback, and a fifteen dollar dispute fee.

- On the day of the sale, the journal entry debits Shopify Payments Clearing for the full ten thousand and distributes credits across Sales Revenue for nine thousand two hundred, Sales Tax Payable for six hundred fifty, and Shipping Revenue for one hundred fifty.

- When the chargeback notification arrives, the disputed one hundred fifty dollars debits to a Chargeback Reserve asset account, the fifteen dollar dispute fee debits to Merchant Dispute Fees expense, and Shopify Payments Clearing absorbs a one hundred sixty five dollar credit for the combined total.

- When the net payout deposits to the bank, the operational checking account receives nine thousand five hundred forty five dollars, Merchant Processing Fees expense captures two hundred ninety dollars, and Shopify Payments Clearing takes a final credit of nine thousand eight hundred thirty five, representing the original ten thousand minus the one hundred sixty five already removed by the chargeback entry.

The clearing account now carries ten thousand dollars on the debit side and ten thousand dollars on the credit side. The balance is zero. The reconciliation is complete.

")

Topic 11: Advanced Solution for Gift Card Breakage

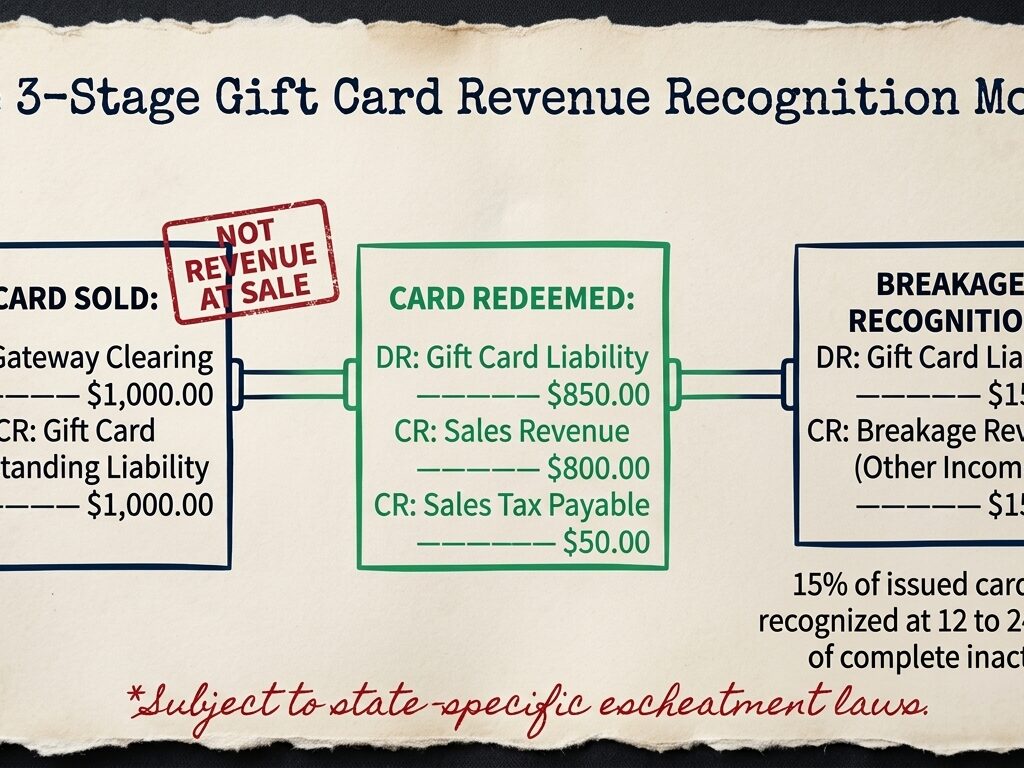

Gift card programs require precise accounting treatment under both GAAP, specifically ASC 606, and IFRS, because the initial sale of a gift card represents deferred revenue rather than earned income. No product has been delivered at the point of purchase, so the transaction records as a liability, not as revenue. When a customer buys a gift card, the entry debits the applicable gateway clearing account and credits Gift Card Outstanding Liability, a current liability on the balance sheet. Revenue recognition happens only at the point of redemption. When the card gets used, Gift Card Outstanding Liability gets debited and Sales Revenue gets credited, along with Sales Tax Payable, because taxes apply at the moment of redemption, not at the moment of the initial sale.

The accounting layer most merchants miss involves breakage, meaning the portion of sold gift cards that statistically will never be redeemed, which historically runs between five and fifteen percent of issued card value. Under ASC 606, that expected breakage must be recognized as revenue over time rather than held permanently as a liability.

Merchants with stable historical redemption data use the proportionate method, recognizing breakage revenue in proportion to actual redemptions as they occur. Newer stores use the remote method, recognizing breakage only when the likelihood of a specific card being redeemed becomes remote, typically after twelve to twenty-four months of inactivity on that card. When that threshold is reached, a manual adjusting entry debits Gift Card Outstanding Liability and credits Gift Card Breakage Revenue in the Other Income category, clearing the balance sheet of a liability that no longer has a realistic redemption expectation behind it.

Topic 12: Summary Mastery Framework Checklist

Every problem in this industry traces back to the same root cause: treating gateway deposits as revenue rather than as the final step in a structured clearing process. The framework that corrects it runs on three rules:

- First, deploy an automated middleware connector, such as A2X or Link My Books, that translates Shopify payout data into batched journal entries rather than individual transaction imports. Stores processing more than one hundred orders per month should not be running direct sync integrations.

- Second, establish a dedicated clearing account on the balance sheet for every payment gateway the business uses. Each clearing account should reduce to zero after every payout cycle, and any non-zero balance at period end is a diagnostic flag pointing directly at an unrecorded adjustment, whether that is a missed fee, an open chargeback reserve, or a BNPL recovery that never received a manual entry.

- Third, verify that the financial statements report gross sales rather than net deposits. Processing fees belong in operating expenses, currency exchange losses belong in their own ledger category, and gift card revenue stays on the liability side of the balance sheet until a customer actually redeems the card.

Merchants who build this structure before they need it, not after a discrepancy surfaces during a tax filing or an audit, protect their gross margin visibility, reduce the time required for month-end close, and build a financial foundation capable of supporting actual scaling. Build the system so the numbers are right the first time.